Here's the latest market news, hand-curated by our research team.

The Big Story

DraftKings rallied 5.6% in premarket following news that the sports betting company is close to signing a new partnership with Walt Disney's (DIS) ESPN division. The agreement would open the door for the media behemoth to profit from the expanding trend of regulated sports betting and potentially help both companies widen their audiences.

• US CPI is likely to capture all attention. Investors who frequently had their dreams dashed for a Federal Reserve turn away from an aggressive rate hike campaign will eagerly await US inflation data on Thursday.

• The minutes of the most recent Fed meeting, which are expected to be released on Wednesday, should reveal how officials perceive the economy and the outlook for inflation.

• Lastly, It is the start of the Q3 earnings season. Much anticipated Big bank earnings (Thursday and Friday) are expected to show the impact of rising interest rates and market volatility.

Economic data this week

• US CPI, PPI, Small business optimism, real earnings, retail sales, Michigan 5-year inflation expectations

• BlackRock, JPMorgan, Wells Fargo, Morgan Stanley, Citigroup, First Republic Bank

• Delta Air Lines, Fastenal

Crypto

• Bitcoin remains unchanged from last Friday, despite falling as low as USD19.3k over the weekend, as traders seek clues whether the selloff in stocks and the rise in the dollar will continue.

• Crypto exchange FTX is the latest to partner with payments giant Visa to issue debit cards for US customers, giving users the ability to use crypto to fund purchases at millions of merchants around the globe.

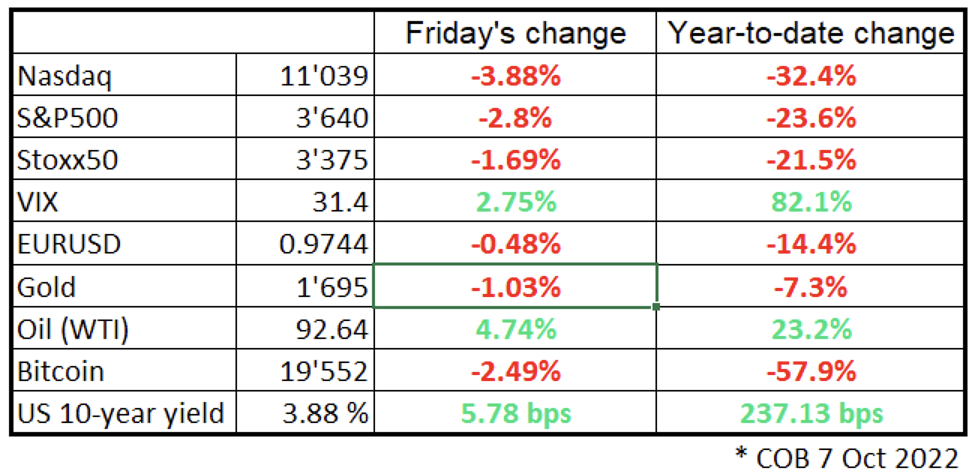

Stocks started last week on a strong note but rapidly came under pressure after bond yields rebounded on stronger-than-expected US September jobs data, suggesting the Fed is likely to raise rates further and for a longer period of time. The oil and gas sector (XLE, +13%) was the top performer, while real estate (XLRE, -4%) lagged behind.

The dollar bounced, erasing early-week losses, and the pound's rally lost momentum, reversing some gains as Truss seems committed to cutting taxes. And, oil prices rose 15% in the week after OPEC+'s output cut.

This morning, risk appetite remains subdued as the outlook of further aggressive rate hikes weighs on markets. Equity futures are in the red, oil is down 1%, and the dollar is holding onto its gains of last Friday.

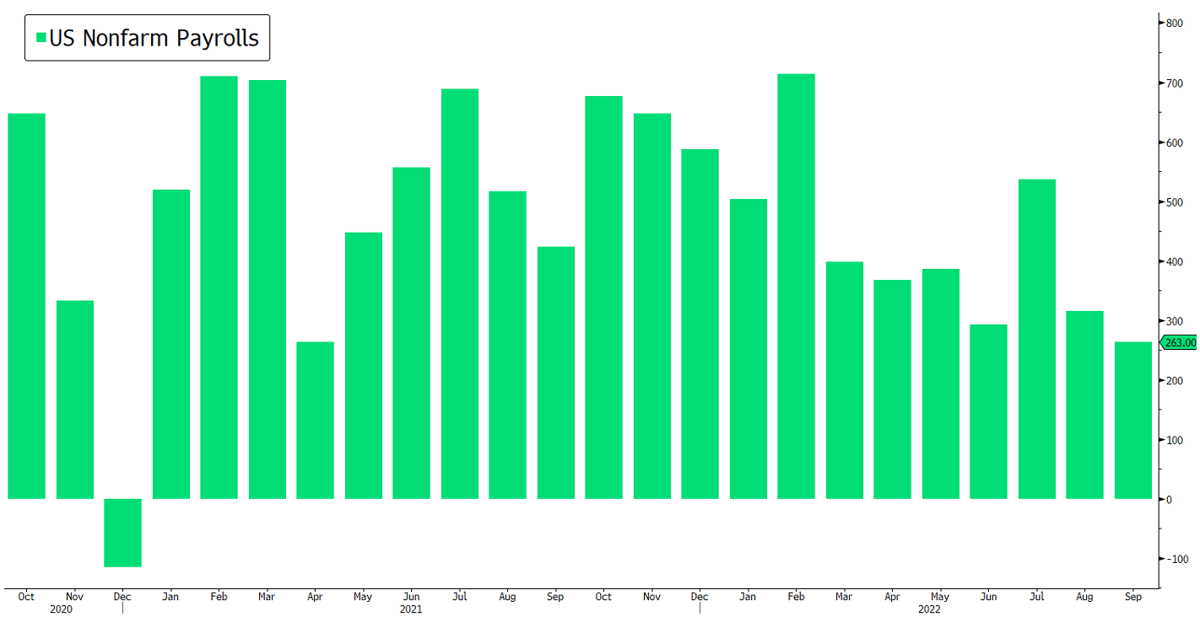

Chart Of The Day

US September jobs growth came above expectation, sending stocks lower as investors bet the Fed will maintain its aggressive tightening monetary policy for longer.

FlowBank Blog

Is Parity Calling for GBPUSD after Mini-Budget Volatility?

It’s been a wild old ride for the British Pound over the last fortnight. It has been brought on by a loss of confidence in the new British government and corresponding trust that the Bank of England can save the day.

This email and any files transmitted with it are confidential and intended solely for the use of the individual or entity to whom they are addressed. If you have received this email in error, please notify us immediately, and delete it from your system. If you are not the intended recipient, you are notified that disclosing, copying, distributing or taking any action in reliance on the contents of this information is strictly prohibited. Although we scan attachments, we advise you to carry out your own virus check before opening any attachment.