1247 days ago • Posted by Charles-Henry Monchau

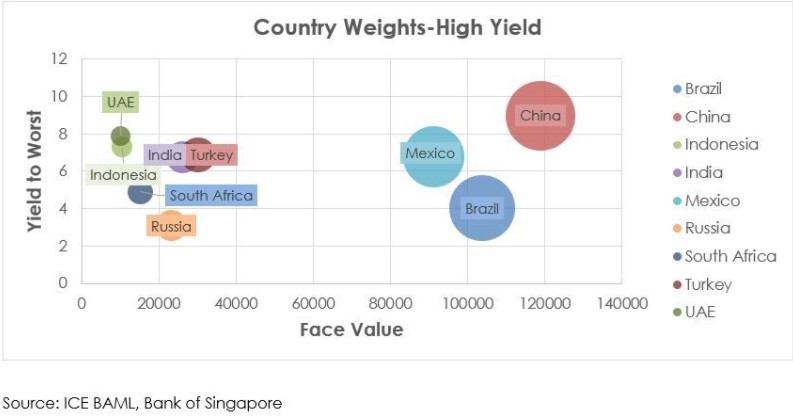

China it the 800-pound gorilla of Emerging Markets High Yield Corporates

"China Yield is not only relatively attractive from a comparative valuation perspective, but its size is hue, particularly for the higher beta portion of the market. Replacing the market yield and index weight of China elsewhere within the Emerging Market Corporate realm is a daunting task to say the least. The greater one underweights China, the larger the number of wide-ranging, idiosyncratic bets one is forced to take. In Asian Credit, the high beta alternatives are often challenged/distressed names in India or Indonesia. This also makes Chinese HY a potentially super-crowded trade going into 2021" - source: Todd Schubert - Bank of Singapore.