It is fair to assume that most of us use some sort of cosmetic or beauty product; perfume, hair gel, face cream, make-up... While it may represent a relatively small fraction of our monthly spending, the recurrence of our purchases translates into one of the biggest markets in the world today.

Key Takeaways:

- There is a strong historical and sociological need for cosmetic products, which could be the main driving force behind a timeless demand;

- The cosmetics sector as a whole is growing double digits with mass market brands seeing sales rise 14% in 2020;

- Social media and streaming has become a mantlepiece of the cosmetics industry upon which brands and consumers meet;

- Millennials don’t see brand loyalty the way older generations do because they have more buying options and care about personalities rather than standalone brands;

- While there are several small and large brands, the leaders are L’Oréal, Estee Lauder, Coty, Ulta Beauty and Proctor & Gamble.

The timeline of cosmetics

From a religious standpoint, makeup first appears in the book of Enoch as a symbol of corruption. The fallen angel Azazel teaches men to make arms and use dyes to beautify their eyes. Corruption ensues and so does chaos…

Clockwork Orange: the main character, who symbolizes chaos, wears makeup.

But in modern times things are different in that makeup does not equal sin as much as it means identity, or from the Greek word ‘’kosmos’’, cosmetics means ‘’to arrange’’.

Cosmetics is a huge industry. Global mass beauty and personal care sales amounted to $307B and skin care sales saw $145B in 2020. According to industry experts, the market is coming to a sort of equilibrium with the TikTok era, where the focus is shifting towards social media celebrities like Yuya, Jeffreestar and Musas and large cosmetic firms start to dominate smaller niche players.

Industry and brand momentum acceleration

Industry growth has sped up in 2020, partly due to the pandemic though not entirely because of it. There was already momentum before covid—one can look at L’Oréal stock price growth as testimony to this trend.

In Q1 of this year alone, firms saw a 13% year over year increase in sales, building on top of an 8% increase over Q4 in 2020. Sales of mass market brands are up 14% year on year in Q1 and both entry-level prestige and high-end prestige brands showed a 12% improvement.

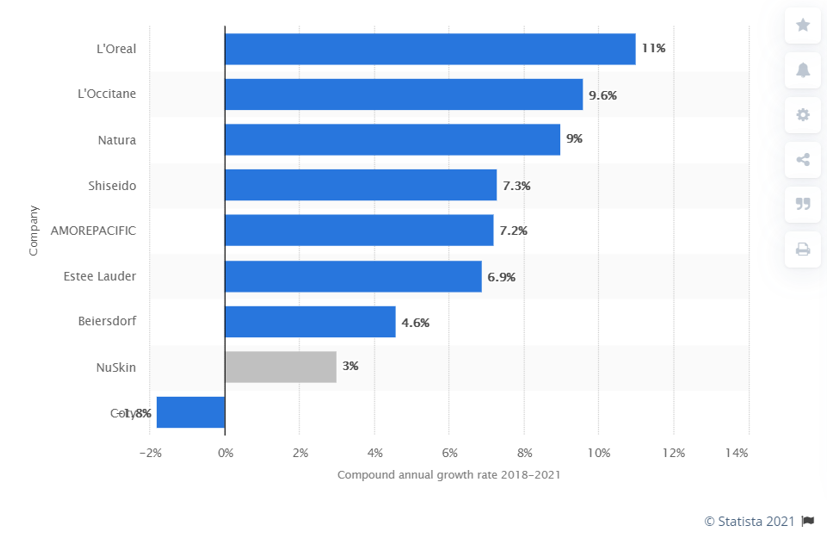

Gross margins are between 40% and 60% in cosmetics (which is huge), and few, but strong firms are leading the pack. The next Statista graphic shows this impressive growth:

Figure showing CAGR of leading cosmetic brands between 2018 and 2021

Four recent drivers come to mind that justify this performance: a boom in e-commerce, streaming, a growing middle class in emerging markets and most recently, extra spending money from the stimulus.

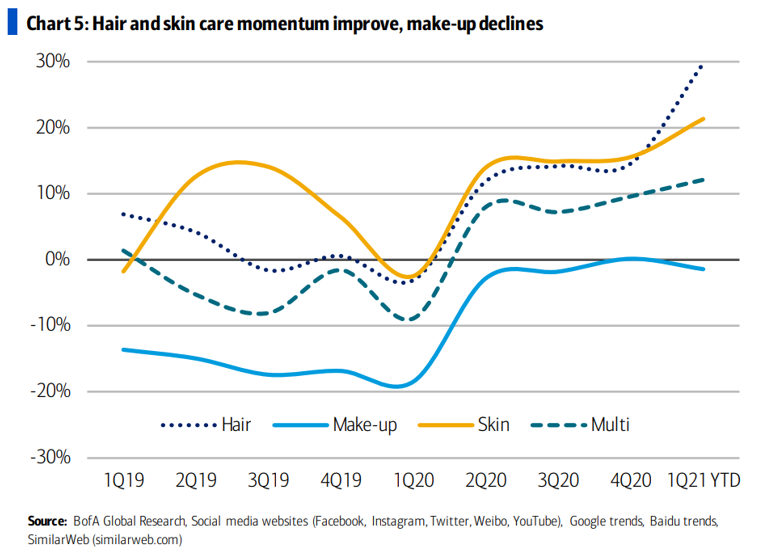

Overall, the money is being made in hair and skin care products, not makeup. As showcased in the graphic below, hair products are on the up with P&G, Henkel and L’Oréal taking the bulk of the market. Skin care takes second place driven by L’Oréal, and Unilever. Make-up has struggled to breakaway since before the pandemic in 2019. However, with a worldwide reopening, some argue that makeup heavy players could see a resurgence as people start going out more.

Figure showing hair and skin care products trends soaring

Segmentation, Norms, and Streaming

While hair products are soaring, marketing specialists have noted that a 4% CAGR per year in the skin care department is encouraging. Skin care was already hugely in demand in Asia due to cultural norms, but with covid, skin care demand has surged outside of Asian markets, in Europe and the US.

Perfume is huge in Europe where France has always been a powerhouse producer. The same cannot be said of Asia where culture norms differ on the use of scent. In Asia, powders to lighten the skin are seen as more valuable than other cosmetics—something completely driven by norms, and not seen in Western countries as much.

The lipstick effect is also something to be aware of. This is the practice that large luxury powerhouses like Hermes and Saint Laurent use to capture more lower-end price consumer surplus; when one cannot afford a Hermes scarf, maybe they will will buy a Hermes perfume instead.

Because of this practice, more luxury brands (even luxury car firms) are entering the cosmetic market via white labels to round off their bottom lines because they see 40-60% gross margins on such products and say, why not. This speaks volumes of the cosmetic industry as a profitable business to be in, and how luxury partners starting to penetrate the market could be good for cosmetic firms.

Influencers have also become a pivotal channel through which cosmetic companies are growing. As seen in the next section, social media, since the advent of streaming, represents a major growth point for top players—the younger generation wants access to educational content, and through it, firms are seeing healthy returns via mobile sales taking off on Instagram and TikTok.

Three Cosmetic Themes

Product InnovationFirms are seeking cleaner formulations as well as eco-friendly packaging and low footprint manufacturing—typical efforts seen by large players trying to capture more demand. Consumer behavior is changing and consumers are becoming more aware of their ecological footprint—what they put on their face should reflect their moral compass. Brands like Procter & Gamble coming out with Olay, and Coty’s Cover Girl are examples of the direction top players are taking to address this changing consumer behavior, but many are still stuck ‘’greenwashing’’ their labels.

Going digitalWhile this is not unique to cosmetics, digitally-enabled brands will be able to capitalize on a wider demand curve. Marketing efforts are increasingly leveraging AI analytics to better understand market segments and pricing, and shoppable live streaming events and interactive tutorial sessions are now normative and sources of profit.

Brand differentiationThe cosmetic business is addressing political change in its products with advertising becoming increasingly inclusive of all genders, identities, and racial backgrounds. In a similar vein to Nike’s ‘’everyone can be an athlete’’ philosophy, large cosmetic firms say that everyone can be more ‘beautiful’. Broadening the market is never a terrible idea, and this only adds to the investment thesis. L’Oréal is a leader within the identity branding theme; others trail somewhat behind.

How to play it

In the US, Estee Lauder dominates other beauty players in the entry-prestige and high-end prestige lines. They have made drastic improvements in their social media efforts where their leveraging of Instagram has given rise to a 55% increase in sales at their Tom Ford brand. Coty’s Wella brand saw much momentum with a 30% increase in web traffic and within the mass market segment, P&G skin and hair care products showed double digits gains as well.

In Europe, L’Oréal continues to govern the market. Their social media presence is soaring placing their brands in the top rankings and figures show yet more rise in the making. L’Oréal have also acquired sustainable companies in order to tap into more brand loyalty potential, but some folks consider this greenwashing more than real ESG practice. Unilever, has seen success in its ‘’beauty with purpose’’ campaign, and ‘’Real Women’’ campaign which saw its Dove brand rise in popularity.

In Asia, Japan’s cosmetic market actually shrank 16% from 2019 according to the Ministry of Economy—blame was put on less inbound demand from falling tourism and an increased work from home pattern. Shisheido is seeing a share price resurgence, however. In China, cosmetic sales on Tmall and Taoboa grew 28.4%, despite an already high base—a great sign. Inverse from European trends, China saw more demand for color cosmetic than skin care products (but only a 4% different in growth).

Other worthy mentions include; Helen of Troy, NU Skin and Ulta Beauty.

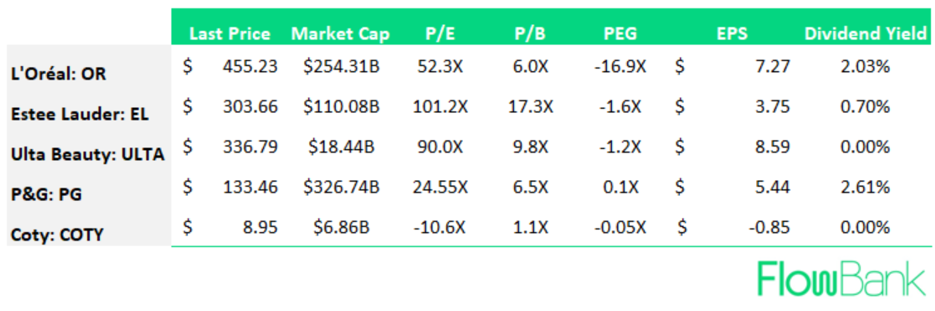

Figure showing top Cosmetic firms financial information