Started in 2011 as a GIF-maker app, Kuaishou became TikTok’s rival in the Chinese short video streaming industry. The app now blends e-commerce, livestreaming, short-form video, and gaming distribution and is preparing for an IPO on Friday with hopes to raise $5.4 billion at a HK$115 price.

Table of Contents

Key Takeaways

- The mobile app is a top outfit in the short video streaming business in China with over 482 million average monthly active users in 2020.

- User metrics indicate that the platform is growing extremely quickly, and perhaps to the demise of its bottom line.

- Operation metrics show that revenues are increasing at a rapid pace, but overall bottom line is slowed by the increasing costs of running marketing efforts.

- Most revenues are generated through digital gifts, but there is an increasing revenue trend coming from running marketing services.

- The biggest risk the app faces is competition from substitute apps and larger players like TikTok.

Business Operations

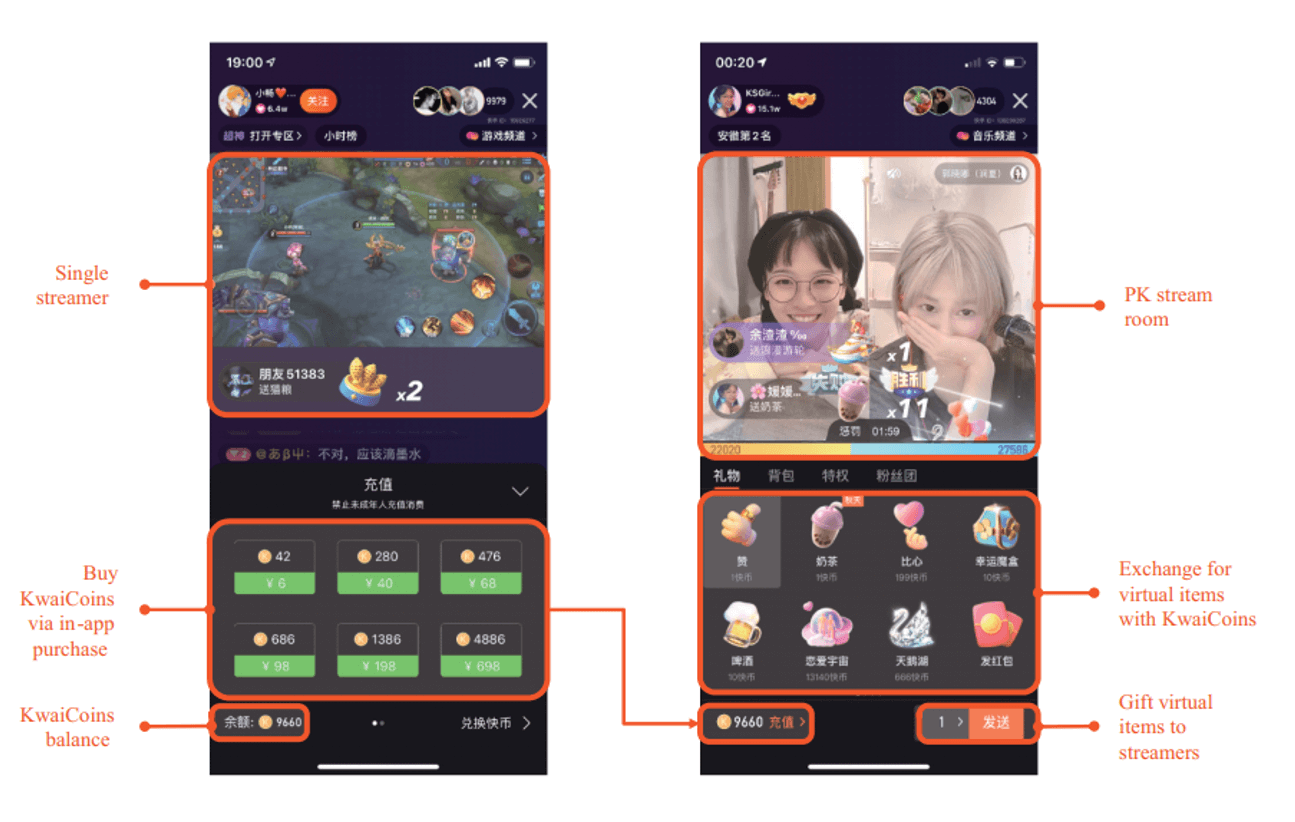

Kuaishou’s business modelKuaishou is a mobile application that enables users to post videos of themselves showcasing skills, products, or anything they like and get paid by the user community. The company’s objective is to generate an ecosystem around content, an ecosystem fit to meet the needs of its users while also offering a commercial opportunity for businesses to advertise their goods.

Kuaishou leverages its large data sets to better serve users with optimized content solutions and aid partners with data analysis for more specialized commercialization of their offerings. Here is a look inside the application:

The mobile video sharing industry is large and could continue to see growth as we say goodbye to 4G and welcome 5G with open arms. China is leading the world in terms of video-based mobile growth. According to iResearch, in 2019, China already had the largest mobile internet population with 873 million internet users. This number is significant as it represented 23% of all mobile internet users worldwide then.

The forecast for China’s mobile internet user base is set to surpass the 1 billion mark by 2025 and see a penetration rate increase from 62.4% to 78.5%. The average Chinese mobile internet user spends roughly 4 hours a day on mobile apps, with estimates suggesting a growth to an average 5.73 hours by 2025.

User metrics

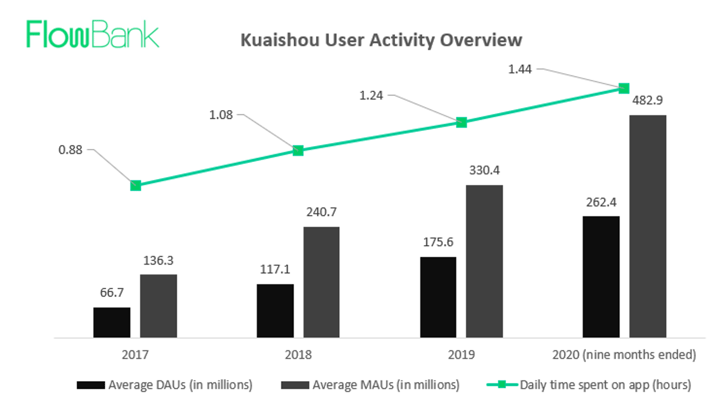

Talking about users, what are the metrics Kuaishou is seeing in activity? Average daily active users grew between 2017 and 2020 from 66.7 million to 262.4 million, and monthly active users showed a similar pattern with larger increases from 136.2 million to 482.9 million. With regards to active time on the application, users have almost doubled their time on the platform over this period which good news for ad agencies who rely heavily on user time exposure to run ads.

Revenue streams and financials

Revenue streams

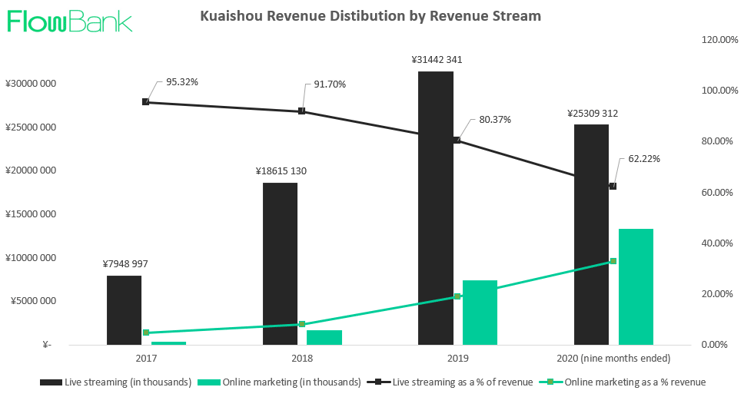

Kuaishou monetizes the app through the sale of virtual items, provisions of various online marketing services and from the commissions gained from e-commerce activity. Kuaishou makes most of its revenues from digital items users buy and commissions made from live streaming; every time a user sends money to another user, Kuaishou takes a percentage of that transaction.

However, the company also generates revenue in the form of online marketing service offerings, and they have seen this segment grow substantially since 2017. In fact, between 2017, and 2020, they increased their online marketing as a percentage of revenue from roughly 5% to 33%, as shown by the green line in the graph below. There has been a trending convergence between the two segments, but nonetheless items and commissions from live streaming still weigh in more heavily on sales. The total e-commerce gross merchandise value blew up from RMB96.6 million at the e-commerce launch in 2018 to RMB204 billion in 2020, and investors should expect more coming.

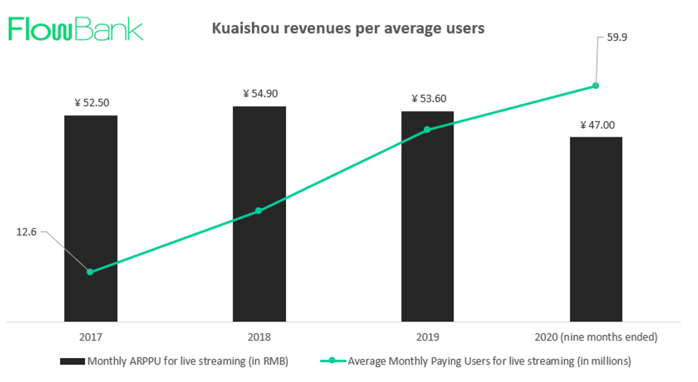

With revenue growth of 143% in 2018, 92% in 2019, and 50% in 2020 we were curious to know how revenues by user has grown. Even though the company has a large active user community of 482.9 million, they show that only 12% of those, or 59.9 million users are active paying users as of 2020. This number has however grown since 2017 when a lesser 9% of users paid. The graph below shows an upward trend in the number of monthly paying users over the past four years and the steady average revenue per paying user of around RMB 52.

Expenses and losses

While revenues have bloated, the company has struggled to keep up with its own growth. The company recorded a loss of RMB 8.9 billion in 2020. Losses from operating the business were primarily attributable to the increased selling and marketing expenses incurred from growth milestones. They attempted to onramp more users, increase engagement and generate more brand momentum to increase market penetration within its competitive industry.

Net loss grew between 2019 and 2020 from RMB 1.6 billion to RMB 97.4 billion. Kuaishou is the victim of its own success, and aggressive marketing decisions, and could continue to see such costs accrue even after the IPO. In all, the Kuaishou IPO could enable them to add some liquidity and continue pursuing branding efforts to tackle rival ByteDance (TikTok).

Risks and weaknesses

Competition is probably the biggest risk facing Kuaishou, because China knows several social platforms built around the short video live streaming business model (TikTok). Their defense is that they believe their user experience is superior because they offer a more diverse universe of self-expression and business opportunity. This also means the firm will have to continue investing capital in marketing efforts to retain users and continue market penetration.

Other risks include:

- Profitability risk. The company has not yet proven it can sustain its expenses even though it is seeing increasing revenues.

- They will need to continue improving growth to continue luring advertisement demand for their platform (which is a growing part of their revenue stream already).

- They are not yet active in other parts of the world; this is a pro and con for the company whereby launching abroad could improve their revenues but also increase their expenses and risk exposure.

- Security and personal data privacy need to be impeccable because users have a fair amount of substitute products to chose from.

Source:

Data, and picture of the app come from the IPO Prospectus found here