Microfinance has the potential to change people's lives and improve women's rights. In this article, we explore what Microfinance is, how it works, why it matters and who benefits from it.

What is Microfinance?

Microfinance refers to financial services provided to individuals who have limited access to conventional banking services such as money holding, loans and basic investment products. It was designed to reach marginalized customers in poorer rural areas from accessing basic financial services given their financial situation or geographic location. Microfinance Institutions (MFIs) are known to be an important global finance innovation as they have significantly eased access to capital among the poorest populations. Despite hundreds of millions of people lifted out of poverty in recent decades, over 2.5 billion people remain with less than $2 a day, and more than half of the world's population, especially the very poor, are without access to formal banking institutions.

Microfinance institutions are like traditional financial institutions in that they intermediate funds between borrowers and savers. All financial institutions must solve the usual issues related to asymmetric information, moral hazard, and payment collection but these problems are particularly distinctive among the poor populations.

Indeed, lending to poor households has always been considered to be doomed to fail as the associated risks are too great, costs are too high and saving propensities are too low. Consequently, poor populations have been excluded from formal financial systems. This exclusion ranges from partial exclusion in the developed countries to full exclusion in lesser developed countries. As a force of circumstance, the excluded populations have developed a wide array of informal, community-based financial arrangements to meet their financial needs.

How Microfinance works

Microfinance englobes several categories of financial services such as microinsurance and microloans, however its most famous one is microcredit. Microcredit consists of extending small loans, called microloans, to impoverished borrowers. These borrowers usually lack verifiable credit history, collateral or even a steady employment. In addition, many of them are illiterate which in turn cannot complete the paperwork required to request a conventional loan. In this view, microcredit was designed to support entrepreneurship and alleviate poverty by offering tailor-made banking services to secluded individuals trapped in poverty who have limited financial resources to do business with conventional financial systems.

As the MFI clientele usually has limited understanding of financial systems, weak legal and political rights and irregular or low incomes, it should be expected that the focus and structure of microfinance institutions will differ from traditional financial services. In this way, unlike traditional banking, MFIs generally do not depend on consumer deposits but rather on small loans relying on social networks and frequent repayments. In this way, they can reduce costs of default, monitoring, and collection. Microfinance is widely considered as a means to help poor individuals manage their finances more efficiently and benefit from economic opportunities while controlling the associated risks. Furthermore, most microfinance organizations exist to fulfill the “double bottom line” of assisting the poor and achieving sustainable financial performance. By offering these financial services, microfinance could help in-need populations out of poverty by promoting economic growth, employment, and economic development.

Why Microfinance matters; The Poverty Trap model explained.

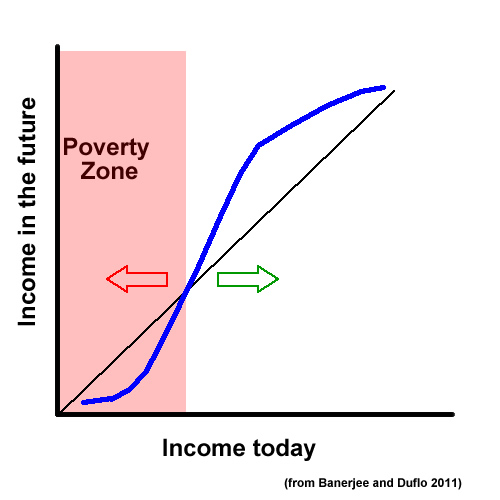

Microfinance is important as it provides resources and access to capital to the financially underserved populations. Without microfinance, these groups may have to resort to using loans or payday advances with extremely high-interest rates which impoverishes them even more condemning them to be trapped in poverty. The poverty trap is a famous spiraling mechanism which forces people to remain poor. It is so binding that it does not allow poor populations to escape from it. The most famous explanation for this poverty trap is access to nutrition. Due to low levels of nutrition, some individuals do not have enough energy to work which in turn decreases their productivity and therefore directly affects their income. This mechanism is called the double feedback loop: a low income leads to poor nutrition which leads to limited working capacity which in turn leads to an even greater fall in income. Nutritional based poverty traps can be explained by using an “S-shape” curve representing the work capacity. The poverty trap zone is the part of the graph for which the intertemporal relationship between the individual’s income today is lower than the next day. Indeed, the amount of money you have today determines what you eat, how much you spend on health, education etc. which in turn impacts your income in the future.

When the work capacity curve is below the 45° line, it indicates that the individual’s income is too low to even feed herself sufficiently. Consequently, she is not as productive which directly affects her future income which will be even lower than the income, she had the day before and so on. All in all, as long as the curve representing the work capacity of the individual remains below the 45° line, individuals will remain stuck in the poverty trap zone.

On the other hand, if an individual lies on the right-hand side of the graph for which the work capacity curve is above the 45° line, the individual’s income tomorrow will be higher than today. Indeed, if an individual has a high enough income today, she would be able to sufficiently feed herself and be productive at work and even save a little for the next day.

Poverty traps can be broken by providing people with the means to earn through investments by offering capital and credit loans. A series of poverty alleviation programs can be enforced to push individuals out of poverty by providing monetary aid for a certain period of time. Nonetheless, if the plan fails, people will become dependent on such programs and may even go deeper down into the poverty spiral. A poverty trap opens the possibility of a “big push” which is defined by a small action which has big benefits, and this is when Microfinance comes into play. Indeed, Microfinance can be considered as the solution for populations trapped in poverty because they can bepushed out of these traps through the helping of financial services specifically designed for them. Microfinance helps them invest in their businesses, and therefore, invest in themselves.

Women and Microfinance

Traditionally, commercial banks have often focused on men and formal businesses, neglecting the fact that women make up a large and growing segment of the informal economy. Female clients have knowingly been disadvantaged in access to credit and other financial services. However, recent studies show that Microfinance Institutions tend to prefer women borrowers. This preference stems from two reasons: women borrowers are considered more trustworthy and reliable in paying back and generally have greater social impact. Indeed, women have consistently registered higher repayment rates than their male counterparts. Therefore, targeting women is considered an important factor for the financial health of microfinance institutions.

“The men were over-confident. But anything the women earned, it went straight to the children. The women always wanted to build for the future. They were terrified they’d lose the money and then no one would trust them again. But the men, they wanted to enjoy the money now.”

Mohamed Yunus (2012)

Moreover, the existing literature has proven that providing financial access to poor women led to the development of the household in general. As a matter of fact, results show that women contribute larger portions of their income to household consumption than the men. As female clients represent 85% percent of the poorest microfinance clients reached, it makes sense from a business standpoint to target them. By the end of 2006, microfinance services had reached over 79 million of the poorest women in the world.

Perks of microfinance:

- Empowering women by enhancing their overall socio-economic status and positively influencing their decision-making power.

- Promoting gender equality by improving working conditions for women.

- Creating sustainable livelihoods for children as they also reap the benefits.

- Increasing likelihood of full-time school enrolment and decreasing the drop-out rates

- Improved health practices and nutrition.

- Programs supporting renewable energy systems and green jobs.

Limitations of microfinance:

- Women have little to no control over their loan with the husband or male family member making all the decisions.

- Gap in literacy, property rights and social attitudes about women may accentuate the already existing animosity towards them.

- Strict repayment approach is adopted given the lack of legit work protocol and verifiable credit history.

- Interest rates remain quite high which is accounted for risk management.

- The scope of microfinance remains small despite its increasing popularity.

Sources:

Banerjee, A. V., & Duflo, E. (2011). Poor economics: A radical rethinking of the way to fight global poverty.

Beck, T., Demirguc-Kunt, A. and Peria M.S.M. (2008). Banking services for everyone? Barriers to bank access and use around the world.World Bank Economic Review, 22 (3), pp. 397-430

Chen, S. and Ravallion, M. (2008). The developing world is poorer than we thought, but no less successful in the fight against poverty. World Bank Policy Research Working paper 4703

Daley-Harris, S. (2007). Microcredit Summit Campaign Report.

Goetz, A. and SenGupta, R. (1996). Who Takes the Credit? Gender, Power, and Control Over Loan Use in Loan Programmes in Rural Bangladesh. World Development, Vol. 24, No. 1: 45-63.

ILO. (2007). Green Jobs and global warming: ILO to discuss new initiatives for tackling climate change in the world of work.

Littlefield, E., Morduch, J. and Hashemi, S. (2003). Is Microfinance an Effective Strategy to Reach the Millenium Development Goals? Focus Note 24, CGAP.

Robin, M. (2012). Lending to women ‘the best decision we ever made’: Grameen Bank's Muhammad Yunus. Women's Agenda.

https://economictimes.indiatimes.com/definition/poverty-trap