Seasonality refers to specific time periods during which stocks, sectors, and indices are exposed to and influenced by repeating tendencies that form patterns in investment valuation. This article will present you some of those historical patterns.

January

The January Effect is the perception of a seasonal boost in stock prices. This bounce is generally attributed to an increase in buying, which follows a dip in prices that occurs in December when investors engage in tax-loss harvesting to offset realized capital gains, which causes a sell-off.

Another argument is that investors use cash incentives received at the end of the year to buy investments the following month. A different theory for the January Effect is that it has something to do with investor psychology. Some investors believe that January is the best month to start an investment program or to keep a New Year's resolution to start investing for the future.

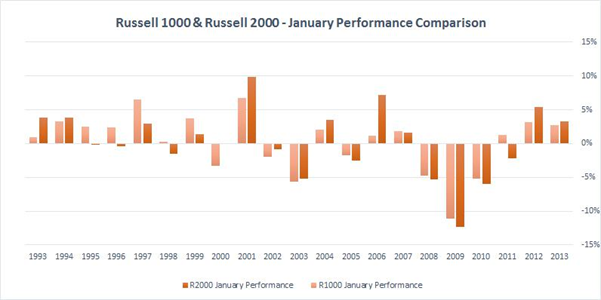

The January Effect appears to affect small caps more than mid or large caps because they are less liquid, as evidenced by historical Russell 2000 and Russell 1000 values. However, because the markets appear to have compensated for this historical trend, it has been less evident in recent years. Here’s a representation of the January performance of the Russell 1000 vs the Russell 2000.

February

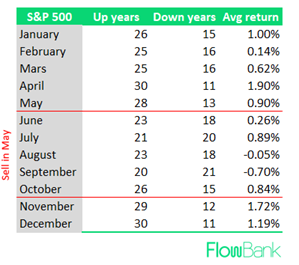

The second month of the year, which is also the shortest, has not fared well throughout history. There's no clear reason for it, but February has historically been a flat month for US stocks during the last 50 years. Only June and September have typically been the worst months.

April

April is often one of the stock market's "highest performing" months. The majority of gains tends to occur in the first 18 days of the month. Monthly S&P 500 seasonality back to 1928 shows that the first 10 sessions of the month tend to be stronger than the last 10 sessions of the month.

May

The phrase "sell in May and go away" is well-known in the business world. It is predicated on equities’ historical underperformance in the "summery" six-month period from May to October, as compared to the "wintery" six-month period from November to April. If an investor followed this plan, they would sell their equity holdings in May and reinvest in November. Some investors believe that this technique is more rewarding than remaining in the stock market all year. They believe that as the weather warms up, low volumes and a lack of market participants (probably on vacation) can lead to a riskier, or at least, disappointing market time. The following figure shows how many times the S&P 500 index was up or down during each month starting from 1980 to 2020, where the theory seems to hold as the June to October period sees lower ups.

August - September

August and September are traditionally one of the stock market's weakest months of the year. Since 1950, the Dow Jones Industrial Average (DJIA) has averaged a 0.8 % drop in September, while the S&P 500 has seen a 0.5 % drop.

The September Effect is a global market oddity that is unrelated to any specific market event or news. Some analysts believe the negative market effect is due to seasonal behavioral bias, which occurs when investors adjust their portfolios to cash in at the end of the summer.

Another reason could be that most mutual funds sell their assets to take advantage of tax losses, and their fiscal year ends at the end of the month. An additional theory points to the fact the summer months usually have lightly traded volumes, as a good number of investors usually take vacation time and refrain from actively trading their portfolios during this downtime.

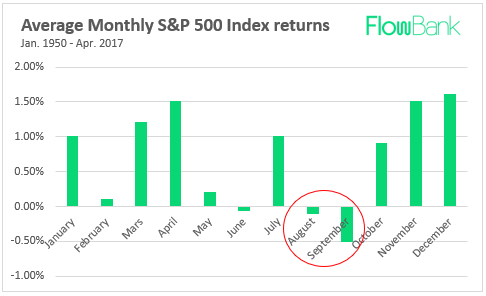

A different idea claims that the summer months have low trading volumes because many investors go on vacation and do not actively trade their portfolios during this time. The following graph shows that both months indeed are the worst performing ones.

October

The October effect is the perception that stock markets decline during the month of October. This effect is primarily a psychological expectation rather than an actual phenomenon as most statistics go against the theory. One thing is true, October is historically the most volatile month for stocks.

The S&P 500 has experienced more 1% or greater fluctuations in October than in any other month since 1950. Some of this can be ascribed to the fact that in the United States, elections are held in early November every other year. The October effect, as well as other calendar anomalies, has seemed to largely disappear over the past decades.

November

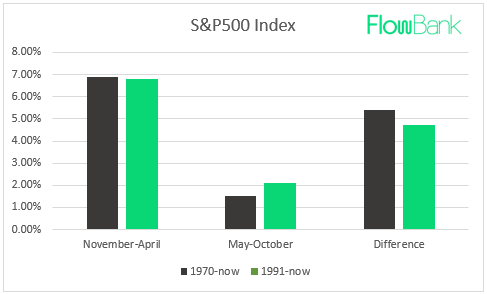

November is the month where the “sell in May and go away” trend ends, the month thus launches the historical best time to invest. The best months appear to be November to April, once the summer vacation time has passed. The end of the year and the beginning of the year are traditionally times when the investment markets are cheerful and enthusiastic. The following chart, with data provided by Bloomberg, is the most effective way to demonstrate this. The statistics are obvious, with an average return of about 7% in the winter months compared to around 2% in the summer.

December

The Santa Claus' Rise, which refers to the stock market's tendency to rally in the latter weeks of December and into the New Year, is the December trend. Increased holiday buying, optimism inspired by the festive mood, or institutional investors closing their books before leaving on vacation are all possible explanations.

The Santa Claus rally, is the outcome of consumers buying stocks in expectation of a gain in stock prices in January, better known as the January effect, seen earlier. Regardless of the rationale, during the 1960s, more than two-thirds of Decembers resulted in positive returns for shareholders. According to some studies, value stocks outperformed growth stocks in December. Still, like with many market abnormalities, it could be purely coincidental, and there's no assurance it'll last.

Conclusion

Using seasonality as a “stand alone” tool to make investment decisions is NOT recommended. Seasonality is an effective analytical tool when combined with fundamental and technical analysis. Moreover, most of these patterns are no longer as performing and as accurate as in the first years when they were found. With investors having more and more access to information it is harder to find arbitrage opportunities especially with such well-known trends that have shown opportunities in the past.

Thus, including seasonality in your strategies can be interesting, however it is not guaranteed to have positive returns, and sometimes even, those returns are not relevant enough as they do not allow you to cover transactions fees.