After a strong year for technology and growth stocks a great equity rotation is taking place. The question is how long will it last? Value and small caps could be taking center stage this year, but not without any drawbacks along the way...

Key Takeaways:

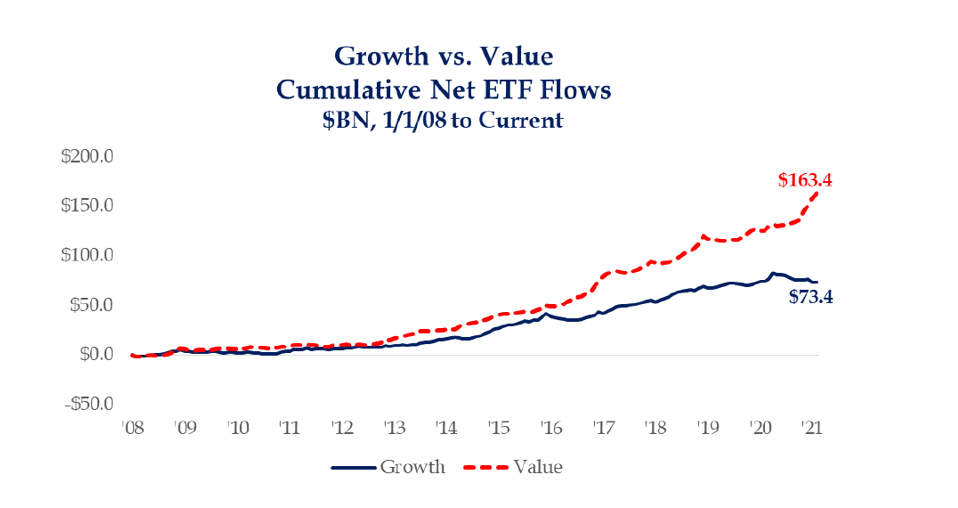

- The Russell 1000 value index outperformed the growth index by 6 ppt or rising 5.8% versus a loss of -0.1% for growth.

- The financial sector has a large weight in value indices and the volatility of energy prices leads to a larger contribution to value performance.

- A combined effect from low yields and a return to GDP growth rates could see the tech sector’s driving earnings through disruptions.

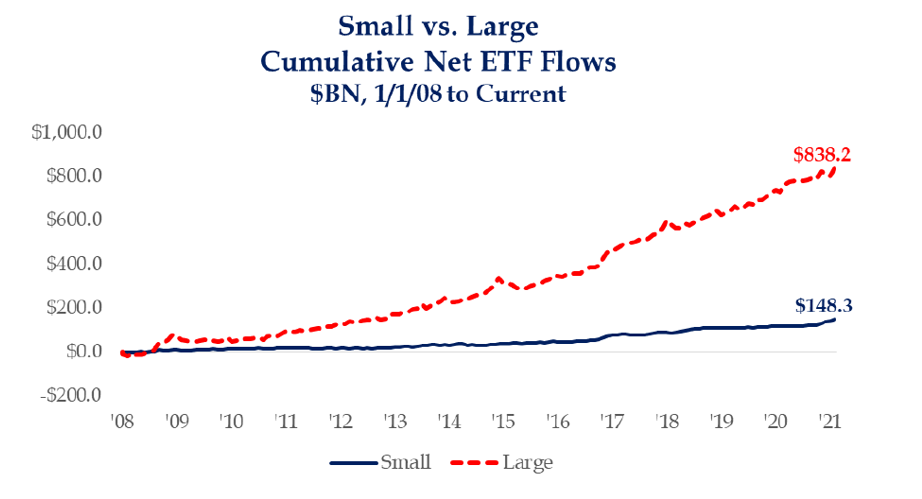

- Large cap ETFs have seen a large spread in the influx of funds relative to small caps.

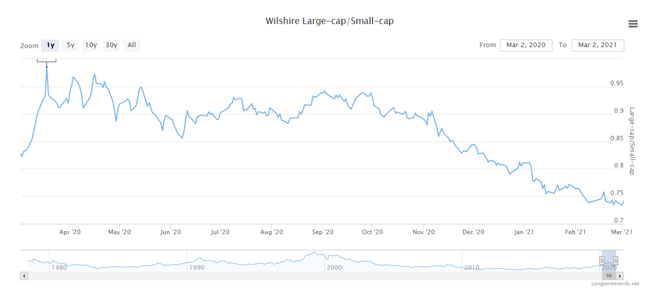

- February saw small caps marked their sixth consecutive month of outperformance of large caps.

- The ratio between large and small cap has been falling.

- Africa’s large materials sector could benefit from further growth and their value equity markets.

What is an equity rotation anyway?

An equity rotation is self-explanatory in that investors pivot from one type of equity to another. Which one to switch over to is what this article explores. In general, the story begins with our position within business cycles. Each industry is subject to its own ups and downs and so is the economy more generally. Industries whose ups and downs are correlated with the general economy’s ups and down are called cyclical stocks. An example of those would be steel or lumber whose demand and therefore prices rise as the economy picks up. Every business follows its own wave called a Kondratieff wave and every operation encounters expansions, peaks, followed by recessions, and later troughs which then lead back to expansions and so on and so forth. The graph below shows a theoretical wave with four phases, and the different asset classes that gain in each phase. We are entering Phase 1, where value and small size firm usually prevail.

With the pandemic we saw expansions in the tech sector, and more specifically the e-commerce and work from home sub sectors of tech. However, some investors see the end of the road as vaccines begin to roll out and economies start opening up. Some argue that valuations have peaked, and that less returns can be squeezed out of certain asset classes. This is why we have seen some tech company share prices fall despite stellar earning reports: great numbers are hard to beat! What exactly are investors considering rotating into and what could be the pros and cons of these rotations?

Should I invest in growth stocks or value stocks?

As inflation expectations and bond yields continue to rise, more focus on value stocks starts to materialize. This is not to say that all growth stocks will underperform, but rather that more gains could be seen in value alternatives. Tax cuts in the US under former President Donald Trump benefited tech companies which happen to have a large weight in growth stock indices.

However, this month paints another picture, a picture of the biggest value rotation since the tech bubble burst. February’s rotation was strong with the Russell 1000 value index outperforming the growth index by 6 ppt or rising 5.8% versus a loss of -0.1% for growth. This represents the best spread since March 2001. While rising rates triggered a rotation, profit cycles, valuation adjustments, and position relative to reflation suggest a champion in value over growth.

The financial sector has a large weight in value indices and the volatility of energy prices leads to a larger contribution to value performance especially as commodity prices rise. In the short term, as bond yields continue their rise and commodity prices keep soaring, the value indices could continue to outperform. There has also been a general trend as shown below of ETFs favoring value stocks since 2013 with net flows rising relative to growth funds flows.

On the other hand, while this rotation makes sense considering short term market dynamics, a partial normalization of valuations could settle. Once valuations have moderated, a combined effect from low yields and a return to GDP growth rates could see the tech sector’s driving earnings through disruptions and present investors with a medium outlook favoring growth stocks over value once again.

Value stock ETFs: SPDR Portfolio S&P 500 Value ETF (SPYV)

Growth ETF: PowerShares S&P SmallCap Materials (PSCM)

Are small caps better than large caps now?

Large cap ETFs have seen a large spread in the influx of funds relative to small caps as shown in the graph below perhaps because the S&P 500 performs well over time (The S&P 500 focuses on 500 large companies). As Warren Buffett says, ‘’never bet against the United States’’. Large caps, strongly driven by S&P 500 weightings, could see further upsides in the coming years despite the equity rotation towards small caps seen next.

February saw small caps marked their sixth consecutive month of outperformance of large caps and represents the longest rally of this sort since the financial crisis. According to BoA research, 84% of small cap active funds outperformed the Russell 2000 benchmark this past month. Furthermore, the Russell 2000’s incredible performance has inspired more attention towards small caps, and rightly so; as seen in the graph directly below, the ratio between large and small cap has been falling suggesting an increase in small cap performance versus large caps over the past 12 months.

Small caps usually outperform large caps during periods of recovery. They should see profits rise should the bounce back be strong and assuming the democrats pass the stimulus pack in the US. With Biden in office, a rising tax could unfortunately slow down the small cap machine, but small businesses should also benefit from a re-shoring in manufacturing and consumer spending in 2021.

Small cap ETFs: iShares Russell 2000 ETF (IWM)

Small Cap Volatilty ETF: VictoryShares US Small Cap Volatility (CSA)

Which is better: emerging versus developed markets

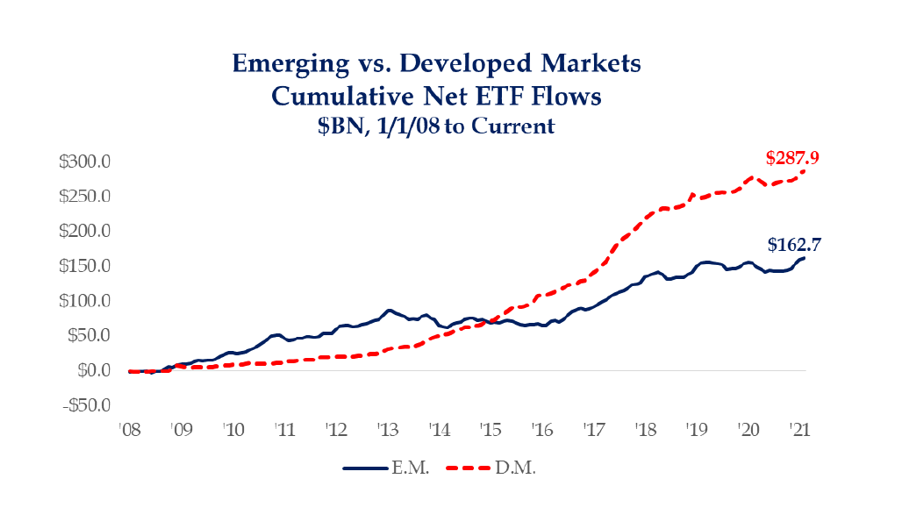

With a commodity super cycle we have not seen in years, we could see an influx in EM ETFs and equities going into 2021, thus reversing the trend showcased in the graph below. But first, the bad news. Emerging nations act completely differently than developed countries in part because of currency credibility or lack thereof. The head of emerging markets economics at Citi writes in the Financial Times that South Africa and Brazil do not have the privilege of exercising monetary dominance in fear of hyper-inflation and soaring debt levels relative to real growth rates. South Africa cannot print money as liberally as the US because it would devalue its currency through price inflation and thus squeeze premiums on their debt and scare off investors who seek compensation. This could help explain ETF flows sticking the DMs.

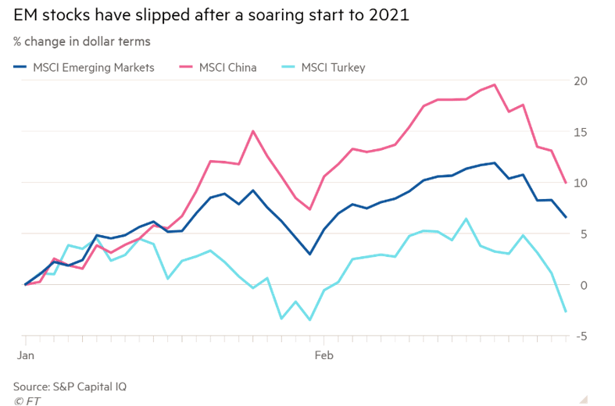

EM stocks have seen a rise due to the pandemic and rising yields according to MSCI’s broad index. This stemmed from investors seeking returns when central bank stimulus depressed interest rates in DMs. The problem for EMs however is that the drop in DM government bond prices (when yields rise, bond prices fall) have sent borrowing costs flying. Even countries like China have seen ripples, despite already seeing signs of a recovery. The CSI 300 Index is up today but has fallen sharply the past couple of weeks. The same pattern is observed in tech focused ChiNext and Turkey’s market.

Despite these constraints, emerging nations offer upsides that could see the above trend reversed. Not all EMs will come out of the pandemic equally strong and most will rely on foreign direct investment to keep growing but some will win. China and India saw surges in FDI in contrast with African and Latin American nations who saw contractions.

However, South Africa’s large materials sector could benefit from further growth and their value equity markets (low valuations) and could also benefit from FDI interested in value stocks as seen above. South African equities have been showed to correlate strongly with overall EM and commodities performance so any positive movements there could be good for those stocks and vice-versa.

ETF on Emerging Markets: Global X MSCI Next Emerging & Frontier (EMFM)

ETF on Emerging Markets Small Cap: WisdomTree Emerging Market SmallCap Fund (DGS)