Here's the latest market news, hand-curated by our research team.

The Big Story

Billionaire Elon Musk notified Twitter late on Friday he is terminating the deal to buy the social media platform for USD44 billion, claiming mainly that Twitter is understating the number of false accounts. The news quickly sent Twitter shares down 5% and Tesla up more than 2% in after-hours, as it alleviated worries Musk would sell further shares of the automaker. The tone of the letter seems Musk wants out of the deal completely and a long legal battle could endure.

•The US inflation report on Wednesday is expected to remain hot, despite recently falling commodity prices. Markets have begun to forecast a slightly more favorable Fed, as inflation expectations fall.

• Consumer sentiment readings in the US and Europe could help shape investors' expectations of the strength of consumer spending.

• Oil traders will eye US oil inventories and the OPEC monthly report. In one month, WTI Crude oil lost 18% and US oil stocks corrected 23%.

• Progressive, Fastenal, Delta Air Lines (Wednesday)

• TSMC, JPMorgan, Morgan Stanley, Cintas, First Republic Bank, ConAgra Foods (Thursday)

• UnitedHealth, Wells Fargo, BlackRock, Citigroup, US Bancorp, PNC Financials, Bank of NY Mellon, State Street (Friday)

Crypto

• Bitcoin broke below its support at USD21'700 over the weekend. Sentiment remains weak as some traders are calling for a further drop.

• Publicly traded Canadian crypto broker Voyager that announced bankruptcy after lending out customer funds to failed hedge fund Three Arrows Capital, attempted to reassure investors "all is not lost".

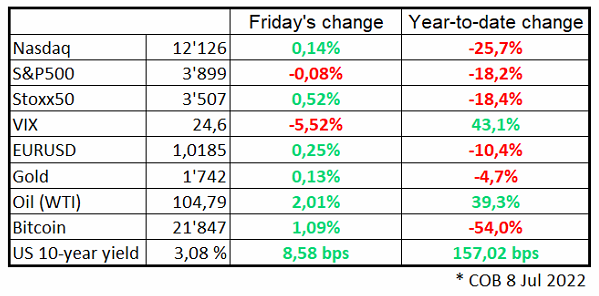

Market sentiment improved last week with the Nasdaq climbing 4.7% and S&P500 rising 1.9%, as investors appear increasingly willing to snap beaten-down stocks. The Nasdaq managed to close in the green for five consecutive days, its longest winning streak since November 2021.

European stocks managed to close 1.7% higher for the week, despite weak economic data and threats of Russia cutting gas supplies. Oil saw a volatile week losing 3.3%. The euro and sterling suffered amid recession fears in Europe and UK political uncertainty. Treasury yields jumped following the stronger-than-expected US jobs report on Friday.

This morning, futures are retreating on fears of more Covid lockdowns in China as Shanghai reported its first case of the omicron. The dollar is higher on risk-off sentiment, ahead of a quiet day.

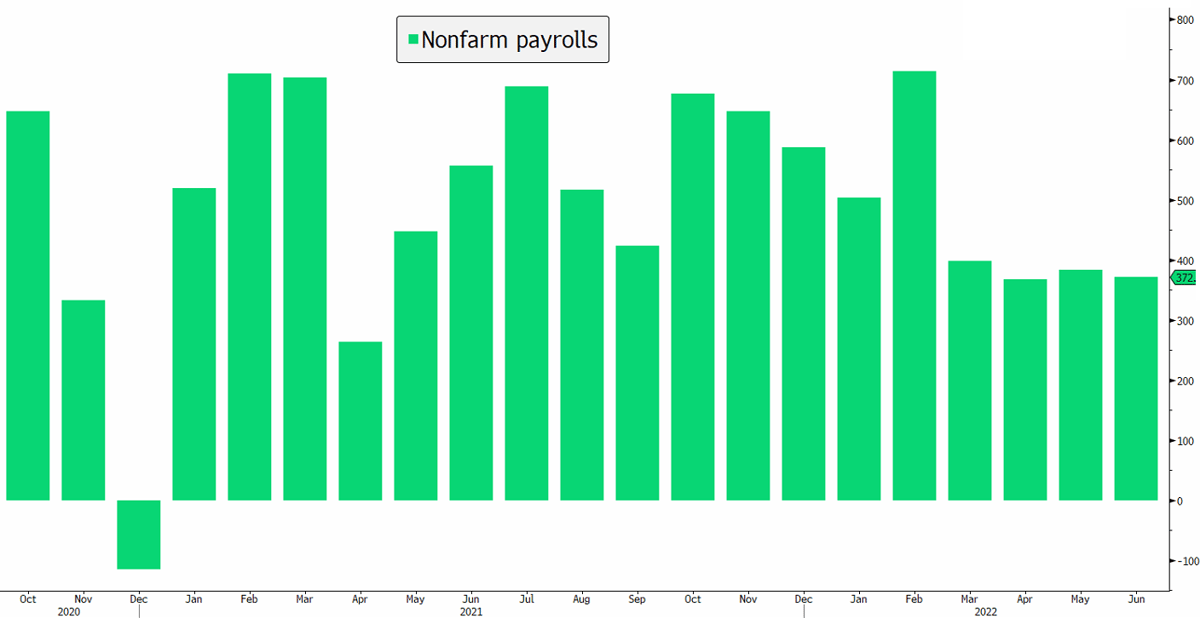

Chart Of The Day

Stocks reacted negatively to a stronger-than-expected US jobs report. It increases the odds the Fed will continue its very aggressive tightening policy, with a 75bps hike in July, which has been weighing on the prices of financial assets. The report is also encouraging as it reduces the fears of recession, which indicates the US economy remains in good shape.

FlowBank Blog

EURCHF Parity Could Signal Further Euro Declines

The steep drop in the euro has come back into focus this week with EURUSD plunging to fresh 2022 lows, now down over 11% on the year. However, perhaps the most notable development is EURCHF holding below parity for the first time since the currency peg was removed in 2015.

This email and any files transmitted with it are confidential and intended solely for the use of the individual or entity to whom they are addressed. If you have received this email in error, please notify us immediately, and delete it from your system. If you are not the intended recipient, you are notified that disclosing, copying, distributing or taking any action in reliance on the contents of this information is strictly prohibited. Although we scan attachments, we advise you to carry out your own virus check before opening any attachment.