It's hand-curated by our research team, and straight to the point.

If you're ready, let's go! 🚀

EM top pick: Energy chaos turns focus to Russia.

The Big Story 💥

It looks like investors are shifting their funds from Chinese assets to energy exporters, with the Ruble posed to benefit from higher oil revenues. Russia's stocks have outperformed relative to the MSCI EM index on bolstered oil prices and prospects of further energy troubles down the line.

Energy prices are pointing upwards in many nations including China and Europe on the back of tight supply chains, earlier and colder winters. Companies in commodity exporting nations will be beneficiaries of a global shortage of supply of power-related commodities.

Russia is the world's biggest energy exporter with a very low debt burden relative to other comparable nations and many asset managers have turned their focus on the energy goliath which is seen in the numbers where Russian markets earnings upgrades have been increasing.

In fact, twelve month earnings projections have increased 14% since H2 in Moscow with rises in oil and energy stocks. High oil prices will continue to support higher earnings and dividends in stocks that make up close to 60% of the Russian index. This would drive the ruble up as investors trade other currencies for ruble to purchase Russian assets which could in turn drive up other domestic industries.

Weekend Action 😴☕

We left off Friday with the energy sector rising 3%, US labor markets reporting improvements in some areas and a debt ceiling that was raised by $480 billion until December 3rd. Today, there isn't a huge amount of economic data on the calendar and the US bond market is closed for Columbus Day.

The market is preparing just days ahead of an important Q3 earnings season kicking off this Wednesday with major banks reporting, and in Europe with LVMH on Tuesday at closing. We expect this reporting period to be noisy considering the August growth slowdown and the September pick up.

Asian stocks climbed today on rallies seen in Japan and Chinese tech and unsurprisingly, crude oil surged beyond $80 a barrel. Japan stocks improved because of a weakened Yen and news that capital-gains taxes would not be changed and net speculative bullish bets on the greenback have improved.

In Evergrande related news, what we see in the markets is a sort of inverse contagion happening between the Hong Kong property index and HSBC stock soaring 17% from recent lows. Looking at high yield credit spreads in China we see property HY spreads widening (more risk) while non-property HY remains narrow.

Also we continue to see a biotech bear-market still looming just looking at XBI which has seen drawbacks relative to the S&P 500. Somewhat related is the healthcare sector as a whole seeing a one month outflow of funds equal to two times the next worst performing sector Staples. Every healthcare subsector is underperforming with tools and biotech struggling the most.

Energy and financials on the other hand have both broken out to new all-time highs. Energy has seen support from rising WTI Crude and rallying commodities. Financials have seen support from insurance doing well and yields pushing higher.

Top 5 Moves 🆕📰

1. Friday's job report wasn't that bad.

The September employment report was a mixed bag. Headline nonfarm payrolls disappointed but the guts of the report were stronger. Delta impacted the data with weak leisure & hospitality jobs and declining labor force participation. Supply-side issues are front and center in this report. While nonfarm payrolls increased only 194K the details of the report were stronger with net positive revisions of 169K and a drop in the U-rate to 4.8%.

2. China coal futures surge to record on heavy flood. In Shanxi China, 60 out of the 682 coal mines have shut due to heavy rains and authorities have said later on Friday that they would consider allowing higher power prices. This region is known for having produced 30% of China's supply of fuel this year. Thermal coal futures have surged to an intraday record today and the government has allowed market action to drive prices i.e. prices could rise as much as 20% for electricity prices.

3. China tech stocks continue their rebound. While sentiment was still high on Monday, the tech index in China remains more then 40% below peaks seen last February--the outlook of the sectors remains blurry. However, tech stocks advanced today in Asia with JD health taking 10%, Meituan 8.7%, and Alibaba 8.4%. Charlie Munger increased his stake in Alibaba by 83% last quarter and overall, stock moved higher on news of a summit between Xi and Biden.

4. Emerson plans a $11 billion merger with AspenTech.

Manufacturing giant Emerson plans to merge two of its software businesses with Aspen Technology in a $11 billion deal. The cash-and-stock transaction would value AspenTech at about $160 per share, according to the report, implying a premium of about 27% to its Oct. 6 close. Emerson would own 55% of the combined company.

5. Germany wants to be the center of lithium production. Rock Tech Lithium (RCK), a cleantech company with offices in Canada and Germany, is planning to build Europe's first lithium converter - a production plant for battery-grade lithium hydroxide - in Guben, Brandenburg. The company intends to locate all production steps of lithium refining in one overall plant at the Guben site. The planned total investment volume at the Guben site for all factory units is 470 million euros and would correspond to the volume needed to equip around 500,000 electric cars with lithium-ion batteries.

Crypto Outlet 🐳

Bitmain, a Chinese manufacturer of cryptocurrency mining equipment, has been forced to stop its business in China from Oct. 11 following the crypto ban imposed by local authorities. In addition to China’s blanket ban on crypto operations, the company has attributed the move to stop shipping Bitcoin (BTC) and cryptocurrency mining rigs as a response to China’s carbon-neutral policies.

Twitter, which has seen its user base steadily grow to surpass 185 million users last year, is experimenting with NFTs to allow users to display their collections as their profile pictures.

XRP has a good chance of hitting $1.50 in the fourth quarter of 2021 after painting a bullish crossover between its 20-day and 50-day exponential moving averages (EMA).

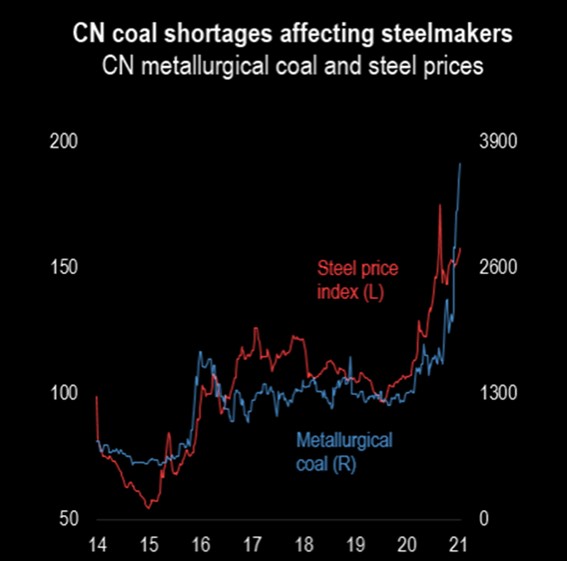

China's energy crisis now sees coal prices soaring

Prices of thermal and metallurgical coal are up nearly 50% since June, fueled by a ban on the import of Australian coal and government-mandated cuts to curb C02 emission. Surging prices are disrupting supply in energy-intensive sectors of the economy like steel manufacturing. China's steel sector is the country's main energy user, relying on coal as a power source and as an input to production.

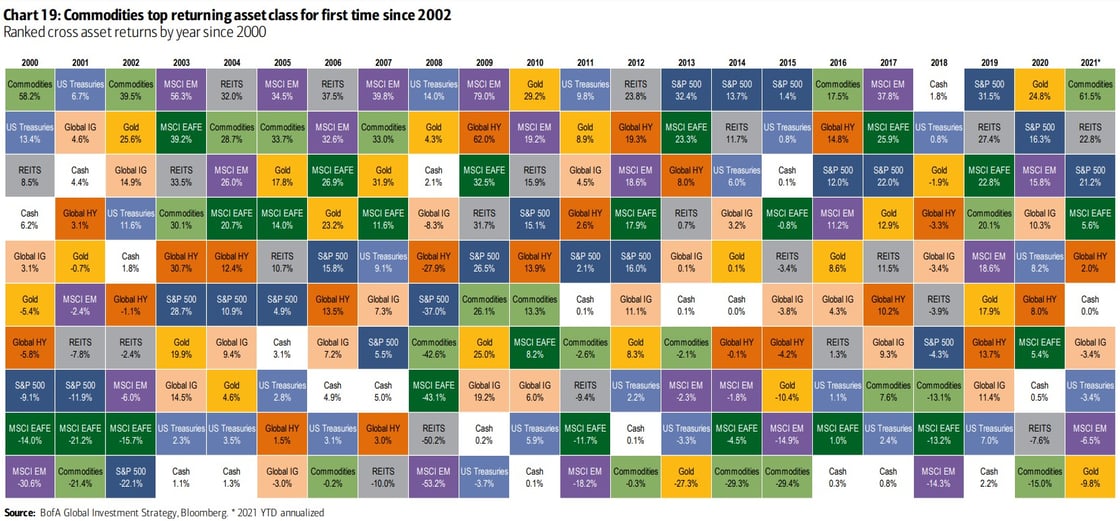

Commodities is top returning asset class for the first time since 2002

Well actually, since 2016, but not at the same level of intensity as we are seeing now. Now, returns are much closer to the bull cycle seen in early 200s when in 2000 commodities returned 58.2% and in 2002, 39.5%. 2016 was a shy 17.5%.

A preview of the news, earnings, and economic data to expect in the week ahead. This week includes the start of earnings season with big banks reporting Q3 results, Federal Reserve minutes as well as US and China inflation stats. The price of oil, which touched a 7-year high last week will likely continue to be a focus point for investors.

This email and any files transmitted with it are confidential and intended solely for the use of the individual or entity to whom they are addressed. If you have received this email in error, please notify us immediately, and delete it from your system. If you are not the intended recipient, you are notified that disclosing, copying, distributing or taking any action in reliance on the contents of this information is strictly prohibited. Although we scan attachments, we advise you to carry out your own virus check before opening any attachment.

.jpg?upscale=true&width=1200&upscale=true&name=shutterstock_1302156640%20(1).jpg)