Here's the latest market news, hand-curated by our research team.

The Big Story

President Biden said Saudi officials share his urgency to increase oil production and foresees further steps in the coming weeks. However, Saudi officials played down the likelihood of an agreement and insisted oil policy decisions would be made within the OPEC+ coalition, which next meets on the 3rd of August. With no immediate supply increase in sight, traders may focus on the demand, still affected by the virus curbs in China and higher prices at the pump following June's price surge.

•Earnings from Tesla, Netflix, IBM, and Twitter will kickstart the earnings season for tech / EVs. Amex, Synchrony, CSX, and J&J should offer insights into the health of the consumer and corporate margins.

• US existing home sales, building permits, and PMIs could signal whether economic growth is slowing down or if momentum remains.

• The euro could face volatility during the ECB press conference Thursday. It could also benefit from a potential reversal in the dollar, which has strengthened to a 20-year high, pressuring the EURUSD.

Economic data this week

• US: building permits (Tuesday), existing home sales (Wednesday), Manufacturing & jobless claims (Thursday), PMIs (Friday)

• Danaher, AT&T, Intuitive Surgical, Newmont, Thales, Pool, Domino's (Thursday)

• Verizon, American Express, Schlumberger, Twitter (Friday)

Crypto

• Ethereum climbed 40% since its July 12th lows, with 12% of gains since Friday, soaring past USD1'400, on hopes for the upcoming Merge. A recent test was successful and the event can be expected for August.

• Investment company NYDIG signed a multi-year partnership with MLB outfit NY Yankees to allow the team's players and staff to convert part of their salary into Bitcoin, in the latest sign of broader crypto adoption.

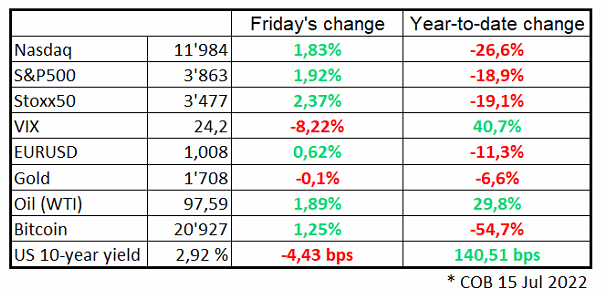

Stocks fell slightly this week on recession fears and following the inflation report on worries it would trigger stronger reactions from Fed officials. Stocks managed to recover most of the losses for the S&P500 to end the week -0.9%, the Nasdaq losing 1.2%, and the Stoxx50 giving up 0.8%.

Oil saw large swings, falling below USD92bp at one point Thursday as traders speculated Middle East producers would boost production but recovered to end the week 6.9% lower. The dollar strength is also a highlight of the week, which temporarily pressured the euro below parity.

This morning, market sentiment is improving as traders slightly reduce bets of Fed hikes and ahead of a busy week packed with earnings. Futures point to European and US stocks opening ∼0.5% higher.

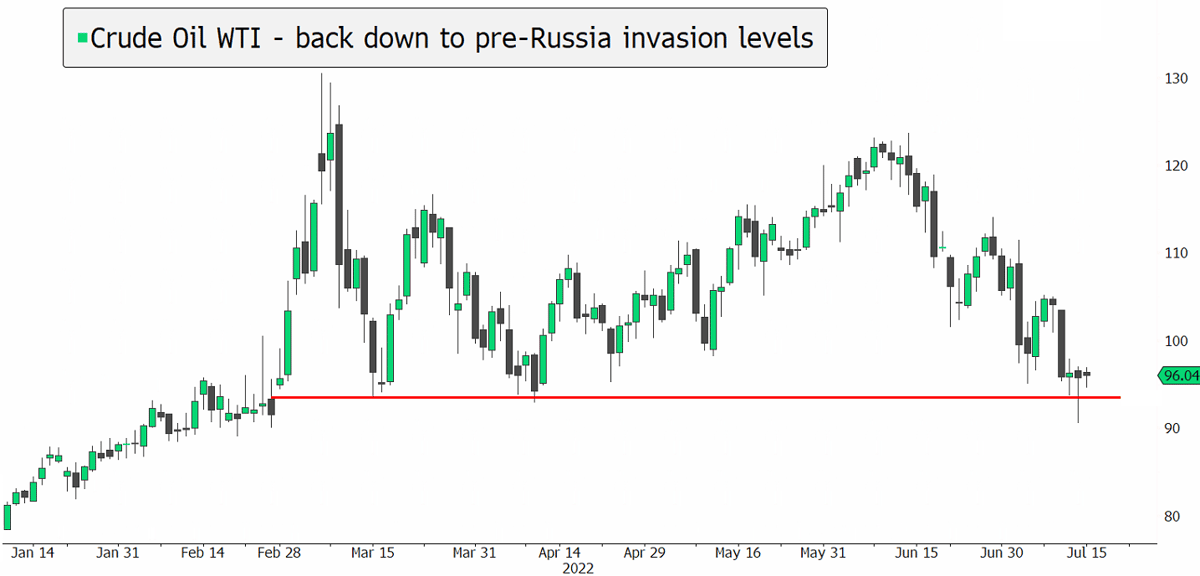

Chart Of The Day

Oil fell below pre-Russia's invasion of Ukraine levels at one point, in a sign that there are serious demand concerns as investors weigh fears of recession as consumers grasp with rising costs, virus curbs in China, and rising interest rates.

FlowBank Blog

Summer Trading: Calm or just the Storm?

With traders in the Northern hemisphere now entering the summer period, a key question is around market volatility. Will market action in July and August be calmer or will the recent volatility continue?

This email and any files transmitted with it are confidential and intended solely for the use of the individual or entity to whom they are addressed. If you have received this email in error, please notify us immediately, and delete it from your system. If you are not the intended recipient, you are notified that disclosing, copying, distributing or taking any action in reliance on the contents of this information is strictly prohibited. Although we scan attachments, we advise you to carry out your own virus check before opening any attachment.

.jpg?upscale=true&width=1200&upscale=true&name=poolside-with-accessories-for-summer-vacations-2022-01-18-23-56-05-utc%20(1).jpg)