Forex Trading: BoE and RBA Join The Summer’s Hiking Club - Outlook for AUD/JPY, GBP/CHF, EUR/CAD

Market Review: What Happened Last Week

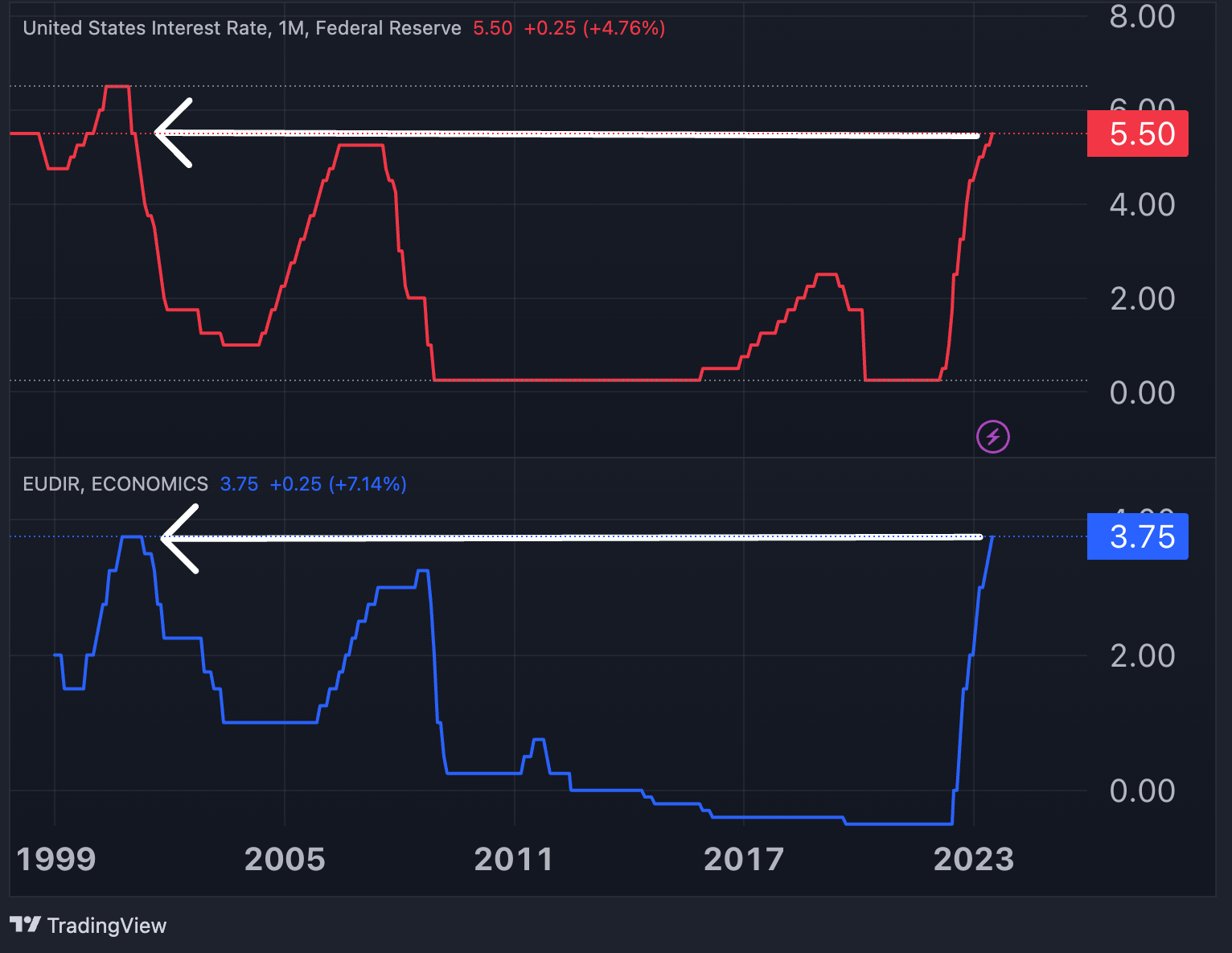

Both the Federal Reserve and the European Central Bank (ECB) raised interest rates by 25 basis points, as anticipated by the market, and announced that future monetary policy decisions will be data-driven. As we head into the September’s meetings, the possibility of further rate hikes or a pause remains uncertain for both central banks.

The real surprise came from the Bank of Japan (BoJ), which announced a modification to its yield curve control policy, introducing greater flexibility to the tool. While the BoJ maintained the "around zero percent" target on the 10-year yield, it loosened the permissible trading band around the target from +/-50 basis points to a softer, non-rigid goal. Initially, the yen rallied on the news, but it later lost ground again as the market realized that the BoJ's monetary policy still remains highly accommodative.

The US dollar emerged as the best performer of the week, gaining 1% against the euro (EUR). The euro closed the week at 1.1015, marking its second consecutive week in the red as Lagarde's remarks on the softening of economic conditions weighed on the single currency’s decline. The Australian dollar (AUD) was the weakest performer among the major currencies last week, falling 1.3% due to weaker export data and a drop in the inflation rate in June to the lowest level since February 2022.

Looking ahead, forex traders will closely monitor central bank meetings in Australia and the United Kingdom, where two rate hikes of 0.25% are anticipated. For the United States, all eyes will be on Friday's jobs report, particularly the highly anticipated non-farm payroll data for July. This crucial release could significantly impact the Fed's interest rate decision in September, leading to substantial fluctuations in the US dollar.

Forex Market: Key Events Of The Week

United States:

- Non Farm Payrolls (Friday): Economists predict a decline in the number of new payrolls in July to 200 thousand from 209 thousand in June. This data is crucial as it provides insights into the health of the labor market, and any significant deviation from expectations could impact the US dollar.

- Unemployment rate (Friday): The jobless rate is expected to remain steady at 3.6%, which is near multi-decade lows.

- Average Hourly Earnings (Friday): Wages are expected to rise by 4.2% year-on-year in July 2023, slightly lower than the 4.4% increase observed in June.

- ISM Services PMI (Thursday): Predicted to soften to 53 from 53.9, indicating a slower expansion in the services sector.

- ISM Manufacturing PMI (Tuesday): Expected to rise to 46.8 from 46, showing some improvement in manufacturing conditions but still indicating contraction.

Euro Area:

- GDP Growth Rate Q2 (Monday): The euro area economy expanded at 0.6% quarter-on-quarter annualized rate in Q2, slightly beating expectations of 0.5%. This marks the lowest pace of economic growth since Q1 2021.

- Inflation Rate for July (Monday): Inflation fell for the third month in a row to a 5.3% annual rate in July, down from 5.5% in June, in line with market expectations. Core inflation held steady at 5.5%, slightly above expectations of 5.4%.

Other Data to Follow:

- RBA Interest Rate Decision (Tuesday): The Reserve Bank of Australia is expected to raise interest rates by 0.25% to 4.35%.

- BoE Interest Rate Decision (Thursday): The Bank of England is predicted to hike by 0.25% to 5.25%.

Chart Of The Week: US and Euro Area Interest Rates Reach Over Two-Decade Highs

New Trades for The Week

Long AUD/JPY

- Entry: 95.05

- Take Profit: 98.7

- Stop Loss: 93.45

- Risk/Reward Ratio: 2.23

Fundamental View

Despite the modification to the Bank of Japan's Yield Curve Control (YCC) policy, the market continues to realize that Japan's negative interest rates weigh heavily on the yen against currencies of central banks raising rates.

This week, the interest rate differential between the Reserve Bank of Australia (RBA) and the Bank of Japan (BoJ) will widen to 4.45%, reaching its highest level since October 2011. This could further strengthen the Australian Dollar (AUD) and potentially retest the June highs at 97.6, with potential to target the September 2022 highs at 98.7.

On Monday, China's better-than-expected factory activity data and new support for economic growth provided a boost to the Australian Dollar, setting a positive tone for the start of the week.

Technical view

The AUD/JPY pair found significant support around the 200-day moving average (91.80) during the volatile session last Friday, from which the Australian Dollar (AUD) rebounded. The relative strength index (RSI) has also turned upwards, surpassing the 50 level, while the moving average convergence divergence (MACD) shows potential for a bullish crossover.

In the past two bullish sessions, the AUD has managed to retrace over 50% of the bearish trend between the June and July 2023 highs and lows. Now, the pair could be heading towards 97.70 (June highs) and eventually 98.70 (September 2022 highs). It's essential to keep the support at 93.45 in mind as the level for the stop loss.

Long GBP/CHF:

- Entry: 1.1185

- Take Profit: 1.1450

- Stop Loss: 1.1075

- Risk/Reward Ratio: 2.54

Fundamental View

The Bank of England is expected to raise interest rates by 0.25% this week, bringing the rate to 5.25%, the highest level since February 2008. Governor Andrew Bailey faces the challenge of addressing inflation concerns as core inflation remains at 6.9%, close to the record high of 7.1% observed in May. Despite some recent softening, there is little room for complacency on inflation.

Given the persistently high inflation, it is unlikely that the BoE will adopt a data-driven approach in future meetings and will probably signal further interest rate hikes ahead.

In contrast, core inflation in Switzerland is dropping at a faster pace, currently at 1.8%, which does not warrant aggressive interest rate hikes by the Swiss National Bank (SNB). The SNB is anticipated to make its last hike to 2% in September, leading to a growing rate divergence between the BoE and the SNB in the coming months.

Technical view

GBP/CHF has been trading within a narrow range between 1.10 and 1.15 throughout 2023, with consistent supports found in the area between 1.105 and 1.11.

Given the proximity to the lower boundary of the range, current levels present an appealing entry opportunity for bullish traders. With these factors in mind, it's reasonable to consider a target of retesting the July highs around 1.1450 in the coming months. To manage risk, the stop loss level could be set at the midrange of the strong support zone (1.1075).

Short EUR/CAD:

- Entry: 1.4582

- Take Profit: 1.40

- Stop Loss: 1.148

- Risk/Reward Ratio: 2.7

Fundamental View:

The second-quarter GDP data for the euro area came in slightly higher than expected (0.6% vs. 0.5%), and July's headline inflation met analysts' estimates (5.3%), while core inflation slightly surprised on the upside (5.5% vs. 5.4%).

In contrast, Canada is experiencing economic slowdown, as evidenced by the contraction in GDP in June (-0.2%).

However, recent increases in energy prices might curb the ongoing economic slowdown and provide support for the Canadian Dollar. Oil prices trading above $80 a barrel represent an important bullish catalyst for the commodity-linked CAD.

In July, the Bank of Canada (BoC) indicated that further rate increases are likely in September and that the slowdown in inflation will take longer than previously anticipated.

Technical View:

The EUR/CAD pair appears to have likely reached a top on July 17, indicated by overbought levels on the RSI. A bearish crossover on the MACD on July 24 extinguished any hopes of a bullish flag pattern.

The current trend seems to favor a downward movement in the pair, with the RSI dipping below 50 and the MACD heading towards the zero line.

Additionally, in early July, the pair experienced a death cross when the 50- DMA crossed below the 200-DMA, further confirming a potential bearish sentiment.

In the medium term, a decline towards 1.40 (50% Fibonacci level of the high-to-low range from 2023 to 2022) is foreseeable. Notably, there will be crucial support tests at 1.4270 (38.2% Fibonacci) and 1.4231 (2023 lows) along the way. A stop loss could be set at 1.4805, for a 2.7 risk-reward ratio.

Trades from past weeks:

- Short EUR/USDOpened on July 24 at 1.1085; Take Profit 1.0880; Stop Loss 1.1150; P&L: +0.5%

- Short NZD/CAD: Opened on July 24 at 0.8174; TP at 0.7975; SL at 0.8263; P&L -0.2%.

- Long USD/CHF: Opened on July 17 at 0.86; TP at 0.89; SL at 0.85; P&L +1.2%.

- Long CHF/JPY: Opened on June 19 at 158.58; TP at 171.62; SL at 152.5; P&L +3.11%.

- Long EUR/JPY: Opened on May 8, at 149.16, TP 160; SL 142; P&L +5.2%.