Gold has been trading sideways or down for almost two years, while inflation is at multi-decade highs. Why are safe haven investments and so-called inflation hedging assets performing poorly while global inflation is reaching multi-decade highs?

Gold vs strong US dollar

Gold prices have continued to disappoint since the start of this year, when prices re-tested all-time highs of USD2’050. Safe haven demand driven by concerns over Ukraine and economic uncertainty has been countered by the strength of the US dollar.

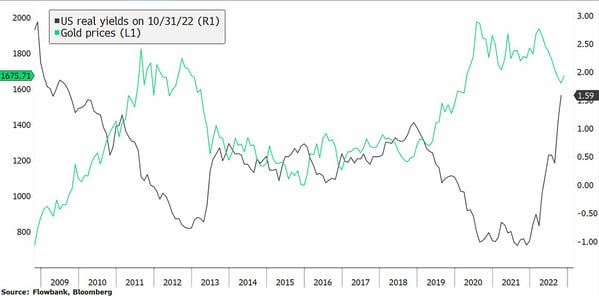

The main driver of gold's decline in recent months has been the US dollar, which has benefited from aggressive Federal Reserve monetary policies. This is in part because higher US interest rates increase the opportunity cost of holding the zero-yielding metal compared to other short term money instruments yielding above 4%. This relationship has been surprisingly consistent throughout history.

For gold prices, this suggests that we are not out of the woods, yet. Lasting high inflation in the US suggest that the Fed needs to keep policy restrictive. In its recent meeting, The US Federal Reserve raised its interest rate by 75 bps for a fourth consecutive time and said that it was very premature to consider pausing rate hikes, adding that officials are strongly resolved to bring down inflation even if this inflicts pain on the economy. Very restrictive liquidity conditions imply more upside risks to US real yields in the mid-term and hence limited upside for gold prices, if not more room to the downside.

Demand unaffected despite global concerns

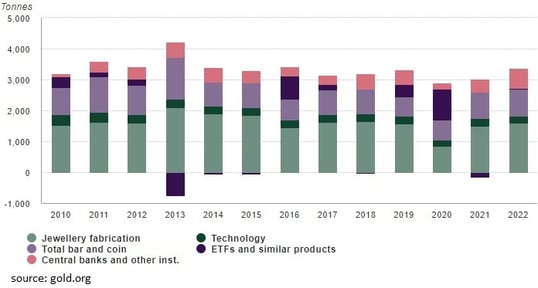

A positive factor for prices is a stronger than expected demand for the bullion. Central banks are hoarding gold reserves. The 400 tonnes of gold purchased by central banks in the third quarter is indeed a record. According to the World Gold Council, these figures represent more than four times the 90 tons of the third quarter of 2021 and almost double the previous record of 241 tons acquired by these institutions in the third quarter of 2018. Among those that may have increased their reserves are Russia, China, and India.

Jewellery demand has also been more robust than previously thought with added support from solid demand in India and other South-East Asian countries. And despite lockdowns and other headwinds, Chinese demand has held up.

So far, central banks have been decidedly hawkish, and in the absence of a U-turn to a dovish tilt, this has clearly increased the risk of moving the global economy toward a mild, if not a deep recession. As a result, we may observe a shift toward safe-haven assets, which would be advantageous for the price of gold.

Technical analysis

A detailed examination of the 2022 chart reveals that as of November 4th, the price of gold -8% year-to-date. While this displeases investors searching for protection, it is important to highlight that gold prices just followed the trend in financial markets. In relative terms, it is still outperforming the S&P500 by more than 10%.

Technically speaking, gold bulls are showing resilience, determined to defend the 1600 - 1620 levels, which is exacerbating bears’ patience, who are looking for a clear drop below this technical support. However, it might not occur right away.

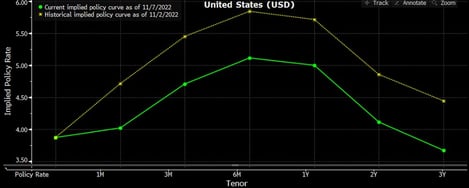

With the dollar weakening and US Treasury rates decreasing due to a lowering in the terminal rate, which fell from 5.8% before last Wednesday's FOMC meeting to 5.1% today, sentiment for rate-sensitive assets improved on Friday. The decline came after some Fed officials suggested moving rates more slowly to balance risks. Gold jumped 3% that day.

The impressive gain could attract more buyers. But how strong and how far this rally can go will be decided near the 1’740 – 1’760 level, where charts suggest major resistance levels.

Conclusion

The recent underperformance of gold highlights its limitations as an inflation hedge. The dollar's strength and interest rate increases have put a lot of pressure on the price of the yellow metal. Nonetheless, despite these liquidity constraints and other headwinds, demand for the bullion has surprised to the upside, driven by strong purchases from central bankers and consumers in India and other South-East Asian countries, a positive trend that is likely to support future prices. While it would be premature to declare that prices have reached their lows, given the extremely negative sentiment, traders could anticipate a short-term rebound.