Microsoft entered 2023 with a bang thanks to its investment in ChatGPT and the surrounding furore over AI.

Still, the company’s top and bottom-line growth indicates prudent financial management in the face of a weakened economy. Likewise, its vast network of AI-based investments means it’s ready to serve growing demand when the sector matures.

What’s happening?

- Microsoft reported revenue growth and successful cost-cutting, driving improved profit margins despite lagging consumer computing sales in the last quarter.

- Microsoft is pouring cash into third-party and internal AI investments and is arguably the best software solution positioned to benefit from widespread adoption.

- At the same time, increased competition might put a damper on Microsoft’s premium-priced products, and increased AI spending means a tighter overall budget.

Fun Fact:

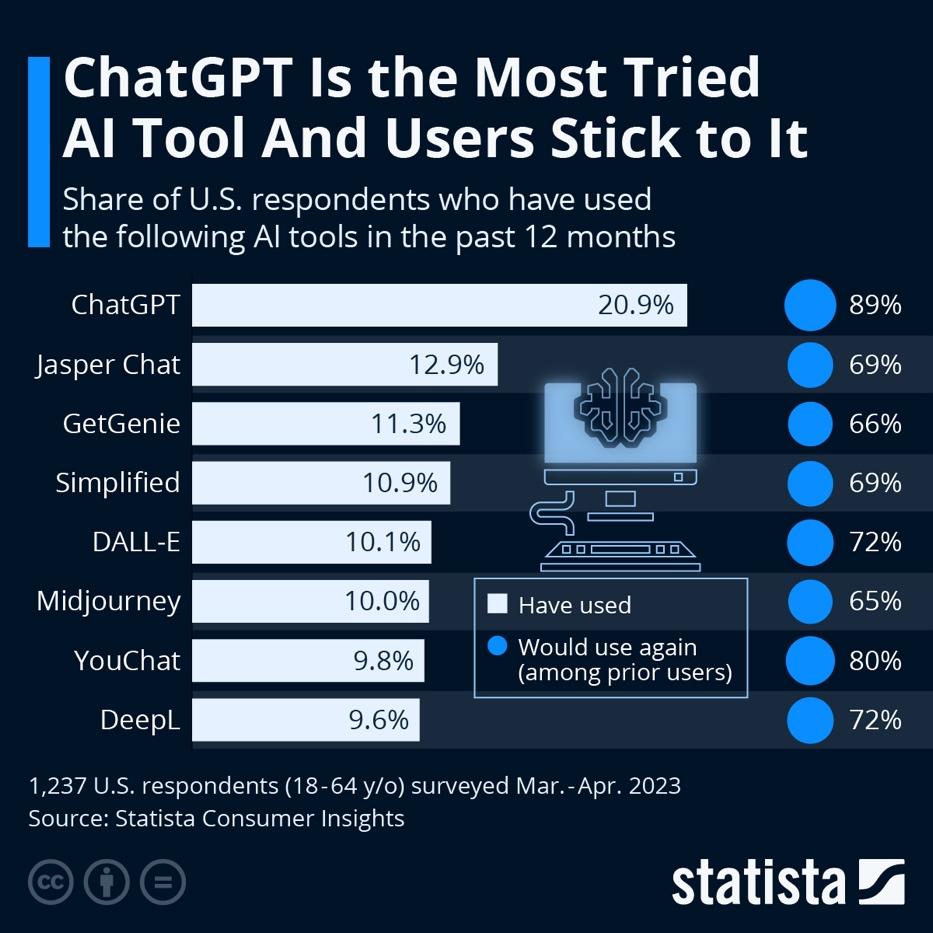

Microsoft invested $10 billion in OpenAI, the creator of ChatGPT. ChatGPT is the most popular AI tool on the market, and users remain loyal even as a flood of competitors comes to market.

At the same time, Microsoft is investing in a host of internally developed AI solutions. Microsoft’s enterprise AI tools are already seeing widespread adoption:

- More than 85% of the Fortune 100 companies use Azure AI.

- GitHub Copilot (an AI-powered coding tool) writes 46% of the platform’s users’ code.

- Microsoft’s AI tools are used by AT&T, General Motors, the NBA, and more.

Microsoft Marked by Modest Growth

Microsoft’s stock is on a run this year, mainly driven by market-wide artificial intelligence (AI) exuberance. AI enthusiasm was triggered, in large part, after Microsoft’s close partner OpenAI unveiled ChatGPT last year. Since then, stocks with even a hint of AI integration have seen their sector surge reminiscent of the mid-to-late-2010s blockchain bull run (anyone remember Long Blockchain Corp, formerly Long Island Iced Tea?).

MSFT returned 33.6% since January. Source: EquitySet

Of course, Microsoft’s diversified services and unique value propositions set it apart from many bandwagoners slapping AI labels on everything possible, like Chegg’s new “AI-powered homework tool.” But, despite substantial stock growth, Microsoft’s recent earnings hit a surprisingly modest tone that could indicate a cap on growth in the near term, if not an outright reversion to the mean.

If MSFT reverted to its pre-pandemic growth trajectory, it’d fall closer to the low end of analysts’ price targets, currently at $232. Source: Nasdaq & EquitySet

For Microsoft’s previous quarter, ending in June, the tech monolith printed 8% year-over-year revenue growth, with their productivity and cloud segments (10% and 15% growth, respectively) compensating for lagging personal computing sales (which hit a 4% drop).

That’s decent, considering today’s economy, but Microsoft’s adept financial management cut costs in this rising rate era and improved its gross margin by 11% and income by 20%. Again, nothing to write home if you’re stacking Microsoft against the hottest stocks in the broad AI sphere, like Nvidia (which doubled year-over-year revenue). Still, Microsoft beat direct competitor Apple, which saw sales revenue slump over the same period.

Microsoft’s Outlook

Microsoft’s short-term outlook is somewhat hampered by its continued direct investment in AI, including its $10 billion allocation to OpenAI. Microsoft is also spreading the love amongst smaller AI startups, including a recent $1.3 billion joint investment in chatbot company Inflection.

At the same time, Microsoft is pouring money into its internal capital expenditure (capex) to expand homegrown AI opportunities. The company’s capex jumped 40% from the previous quarter to $10.7 billion, going into data centers and hardware capacity to support ongoing AI efforts.

As the saying goes, “You’ve gotta spend money to make money,” but the increased capital commitments Microsoft assumes will likely put a short-term hamper on its growth. Still, AI demand is rising exponentially and as one of the first movers in the space, Microsoft’s long-term prospects will doubtlessly pay off, barring any catastrophic constraints (like stringent Congressional regulation some call for).

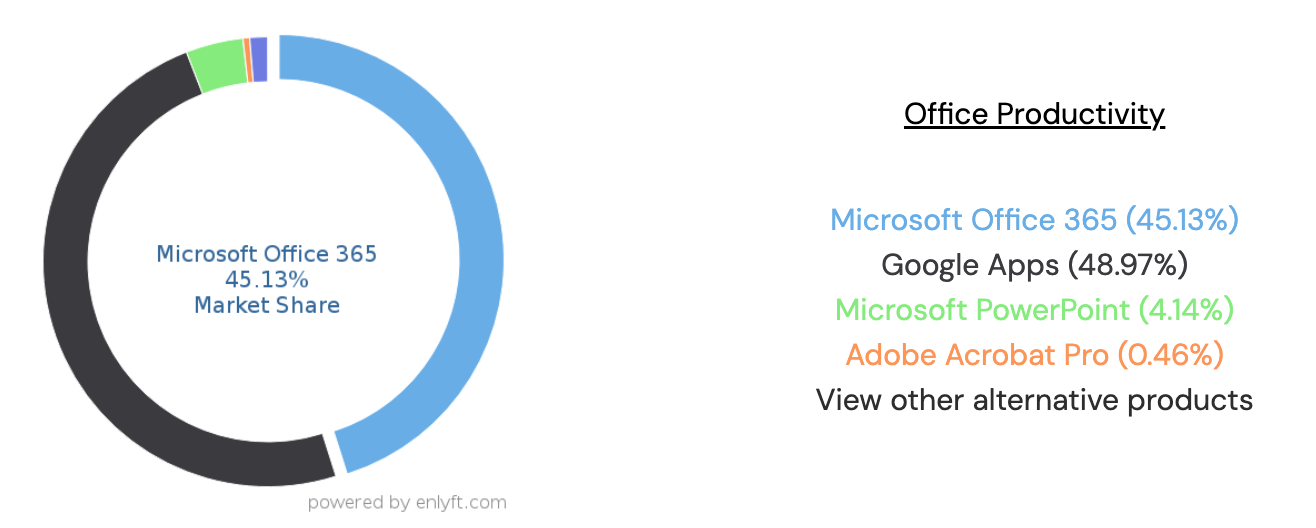

In the meantime, Microsoft’s market penetration is undeniable. As the company’s Microsoft 365 and cloud products dominate corporate spaces, it’s reasonable to assume that high switching costs ensure brand loyalty for, if no other reason, the burden of finding a new provider.

Still, Microsoft controls “only” about half of the total office productivity market, and its competitive edge compared to Google (Docs, Sheets, etc.) is closing. As economic conditions worsen, household users and corporate clients will continue cutting costs, and Microsoft risks losing further cash flow to free competitors like Google.

Source: enlyft

It seems likely that, as Microsoft's AI investments bear fruit, its Office products will become more bespoke and customized to individual sectors, fields, and jobs to create an unproducible network effect to entrench the software in users' hands further. For example, a Bloomberg-integrated Excel add-in already ports data from the legendary Bloomberg Terminal platform. For those using them, Bloomberg Terminals are indispensable, and Microsoft's integration firms up Excel's position within that closed-loop system.

Now, imagine the possibilities with expansive AI embedded – individual firms can train models on their proprietary data, text, or information within Office 365 to create a customized version of Word, Excel, or PowerPoint.

Of course, there's precedent for this already within Microsoft's storied history – remember Clippy, everyone's (least) favorite Microsoft assistance tool?

Now imagine a Clippy that's actually useful and generates insight for your project in real time based on raw data you fed it. That's already the direction Microsoft is headed in, and it's only a matter of time before one of its many invested assets strikes gold.

Short- and Long-Term Potential

Ultimately, Microsoft’s future is bright. It’s racking up financial wins in a constrained economy and pouring money into a new product concept already proven to have near-endless demand for many specific use cases. Still, that forward-thinking perspective comes with a tangible cost as Microsoft pumps cash into its AI investments.

Ramping up those costs means that, in the short term, Microsoft will likely lean itself out further to maintain a cash cushion in case the economy worsens. At the same time, increased free and freemium office productivity tools are encroaching on Microsoft’s territory. If the soft landing doesn’t pan out, Microsoft might be in a bind between its cash outflow and consumer movement towards affordable options as they mind their budgets.